|

CSX still not back on track

|

|

June 28, 2000: 10:08 a.m. ET

Icahn target still hit by service, earnings woes more than a year after merger

By Staff Writer Chris Isidore

|

NEW YORK (CNNfn) - CSX Corp., the rail company that's financier Carl Icahn's latest target, may be getting back on track for earnings growth in a bid to boost its sagging stock price. But its performance on those measures remains a train wreck.

More than a year after it integrated about half of the former Conrail into its rail system, CSX is still struggling to provide the service levels demanded by customers. It is even farther from delivering the profit margins expected in the industry.

A Securities and Exchange Commission filing released late Tuesday revealed Icahn's plans to buy up to 15 percent of CSX, which is trading near lows it hasn't seen in nine years. A statement from the company said Icahn told John Snow, CSX chairman and chief executive, that he has no plans for the railroad, but that he sees the stock as undervalued.

Shares of CSX gained 2-3/16, or 11 percent, to 22-3/4 in trading early Wednesday.

The Richmond, Va.-based company released a statement in response to Icahn's filing saying that it had met with the financier and had decided to strengthen its anti-takeover defenses. It lowered the threshold of ownership to 10 percent from the previous 20 percent level that would trigger a shareholders rights plan, which makes an acquisition more costly.

Icahn's interest seemed to catch the railroad and analysts by surprise, as the sector has seen little deal activity except between railroads. But the low stock price and operating problems at CSX are well known and, unfortunately for its shareholders, well entrenched. Icahn's interest seemed to catch the railroad and analysts by surprise, as the sector has seen little deal activity except between railroads. But the low stock price and operating problems at CSX are well known and, unfortunately for its shareholders, well entrenched.

Analysts who are bullish on the stock say its operating statistics finally show it has turned the corner on service problems within the last few weeks. But even they don't believe that a financial rebound is imminent.

Signs of service improvements but profits still slim

"CSX is improving service, but at a tremendous cost," said Douglas Rockel, analyst with ING Barings, who has a "strong buy" recommendation on the stock but who recently lowered his earnings estimates for the current quarter. "If they get back to the (profit margins) they used to have, earnings per share could be $4 to $5 per share (annually). The question is when? Is it three years away from now? Probably."

Analysts surveyed by First Call now expect the company to report earnings of 28 cents a share, down from 45 cents a share a year ago when the problems with the Conrail merger was already hitting results. More than half the analysts have reduced earnings estimates for the quarter within the last month.

For the year, the company is expected to earn $1.63 a share, up slightly from the $1.59 a share earned during a troubled 1999. And forecasts call for that to rise only to $2.65 a share in 2001.

Many analysts say company projections of keeping operating expenses to 80 percent of revenue or less by the end of the year are probably no longer realistic. That ratio, known as operating ratio, is a key measure of a railroad's financial performance. Many analysts say company projections of keeping operating expenses to 80 percent of revenue or less by the end of the year are probably no longer realistic. That ratio, known as operating ratio, is a key measure of a railroad's financial performance.

"For the full year 2001, you're talking an 82 percent operating ratio, down from 86-and-change in 2000, and better than 90 percent today," said Jim Higgins, analyst with Donaldson, Lufkin and Jenrette.

The rail analysts generally believe the company is making the difficult improvements in operations and service that are required.

Railroad says it is back on right track

CSX officials point to improvements in statistics -- such as average train speed and time spent in rail yards by locomotives and freight cars -- as proof that a new emphasis on service. Its performance of key measures are now near or better than targets set by the company in April, when it shook up top management, said railroad spokeswoman Kathy Burns.

But while the railroad is releasing a lot of operating statistics, on-time performance is one measure it is still keeping to itself. And even Burns admits that service levels have yet to reach where they need to be.

"We knew we're not meeting expectations, nor were we meeting our own," she said. "Obviously our customers have to be the ones to tell us if the service is improving to the level that meets expectations."

Some of those key customers are far from satisfied at this point, especially since CSX is also implementing rate hikes of about 8 percent on much of its commodity traffic before it completes the service improvements.

"If their (operations) numbers are looking better, it's only because they were so bad," said Ed Emmett, president of the National Industrial Transportation League, a trade group made up of the major customers of rail, ocean and motor carriers.

The rate hikes are also criticized by Linda Morgan, chairman of the Surface Transportation Board (STB), the successor to the Interstate Commerce Commission that oversees rail regulation, even though she acknowledged it and other railroads are seeing increased labor and fuel expenses. The rate hikes are also criticized by Linda Morgan, chairman of the Surface Transportation Board (STB), the successor to the Interstate Commerce Commission that oversees rail regulation, even though she acknowledged it and other railroads are seeing increased labor and fuel expenses.

"I've said privately to the railroads, whatever the justification for the rate increase, the timing is not particularly politic," she said.

Morgan said that it is too soon to say that recent improvements in CSX service have let it turn the corner on problems.

"CSX has shown improvement, no question about it," she said. "The question now is will it be stable and fluid and reliable into the future?"

Dropping some business in effort to improve

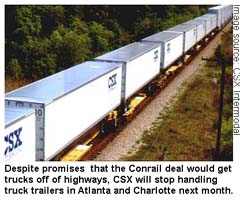

Some of the effort to improve service means walking away from business. Both Emmett and Morgan say they are concerned with CSX's decision to stop taking truck trailers on its rail cars to or from Atlanta or Charlotte, one of the types of rail freight known as intermodal traffic, starting at the end of July.

"I'm going to watch like a hawk that they are taking trucks off the highway," said Morgan. "That's one of the reason we approved the merger." But she said she understands the need to remove the congestion in traffic in and around Atlanta.

Railroad officials insist stopping that trailer service is the best way to improve service for more profitable freight, even if it means losing business to trucks and rail rival Norfolk Southern. They say it will allow them to concentrate on moving containers, rather than less efficient trailers, on intermodal trains in those lanes, as well as clearing the way for longer-haul intermodal traffic from Florida to the Northeast.

"It's an effort to concentrate our strength, on what we do best, and to get away what we don't do as well," said Dan Murphy, spokesman for CSX Intermodal. "It's an effort to concentrate our strength, on what we do best, and to get away what we don't do as well," said Dan Murphy, spokesman for CSX Intermodal.

The head of a major intermodal marketing company, which brokers much of the intermodal freight placed on railroads, agrees with Emmett that CSX service is not showing the improvement suggested by its numbers.

"We're not seeing the on-time performance they're talking about," said the executive, who spoke on the condition his name not be used.

Even bullish analysts such as Rockel say that decision to cut intermodal offerings in the Southeast highlights the overcapacity of much of the nation's current rail system, and why gains in traffic are difficult to achieve.

Still, despite all the criticism and problems, analysts say some short-term rebound in stock price might be seen once investors are convinced the railroad is starting to climb out of its troubles. They point to a rebound in Norfolk Southern stock earlier this year, when service improved ahead of an earnings turnaround.

An end game in rail mergers looms

But how long CSX has to fix these problems as an independent company is uncertain.

A final round of railroad consolidation in North America may well have begun last December when Burlington Northern Santa Fe Corp. (BNSF) agreed to merge with Canadian National Railway Co. (CN) That move is temporarily on hold after the STB ordered a 15-month moratorium in March on railroad mergers while it considers new criteria for approving deals.

CSX and most of the other major railroads pushed for the moratorium, arguing that it was too soon for them to be pushed into mergers themselves. But BNSF and CN fought the STB's order, and the U.S. Court of Appeals heard the case on June 13.

A decision could come any day, and most analysts believe Union Pacific Corp., BNSF's major competitor in the Western United States, will move to buy one of the two Eastern railroads within weeks after the lifting of an order.

Even if the moratorium runs its course, there is likely to be moves to purchase the two eastern railroads sometime in 2001.

Neither of the merger scenarios may help Icahn in his effort to buy shares of the company. His filing with the SEC announcing his interest in CSX prevents him from buying shares before July 12, according to one analyst who asked that his name not be used. The Court of Appeals is expected to rule on the rail merger moratorium by then. Neither of the merger scenarios may help Icahn in his effort to buy shares of the company. His filing with the SEC announcing his interest in CSX prevents him from buying shares before July 12, according to one analyst who asked that his name not be used. The Court of Appeals is expected to rule on the rail merger moratorium by then.

If the court lifts the moratorium on mergers, CSX is expected to be in play from other railroads before Icahn has a chance to buy additional shares. If it does not lift the freeze, he is buying into an industry that will have few takeover opportunities for the foreseeable future.

The Conrail deal is not even the most recent major transaction for the corporation. Last year it sold its international container shipping operation, known as Sea-Land Service Inc., for $800 million to Maersk Line, the Danish ocean carrier with which it had an alliance.

But at the time of that sale it held onto the part of the shipping operation that handles the regulated ocean traffic between the continental United States and other U.S. possessions, as well as a unit that operates ports around the world.

Because of the regulatory restrictions and red-tape involved in rail mergers, analysts said they were surprised that Icahn would become a player in the sector. But one analyst suggested that the rail business might not be his focus.

"You really can't put a railroad in play in an traditional sense," said DLJ's Higgins. "But he could be trying to prompt other changes. There are two attractive pieces of Sea-Land left. This could accelerate their interest in selling that."

Icahn's office had no immediate comment Wednesday on his plans regards to CSX.

As far as a rail merger, some believe that CSX management will try to reject takeover overtures from other railroads if the moratorium is lifted because of its current depressed share price.

Mike Lloyd, analyst with Deutsche Bank Alex. Brown, says such a strategy is risky because a suitor would likely turn to Norfolk Southern. Whichever Eastern railroad is bought second loses a lot of leverage at the bargaining table in an attempt to get a takeover premium, he said.

"Would you be better served from a shareholder value standpoint to just say no?" Lloyd asked rhetorically. "Then you basically force UP to go to the other target. So the question is does the last girl to the dance get the most unattractive date from a pricing standpoint? I don't think it's a disadvantage to wait, but there are smart people who disagree."

-- Click here to send email to Chris Isidore

|

|

|

|

|

|

|