|

Why a rollover may be bad

|

|

August 29, 2000: 6:19 p.m. ET

Once outside a 401(k), your money is more vulnerable to creditors

By Staff Writer Jeanne Sahadi

|

NEW YORK (CNNfn) - There are certainly advantages to rolling over your 401(k) into an IRA. Greater investment flexibility is chief among them. But there also may be a distinct disadvantage. Money in an IRA is more vulnerable to claims made by creditors if you file for bankruptcy or are sued.

That's because IRAs, unlike 401(k)s or other employer-sponsored pension plans, are not protected by the Employee Retirement Income Security Act. ERISA, among other things, insures that money currently invested in a plan for the explicit purpose of your retirement is protected from people to whom you are indebted.

Partial protection in bankruptcy

State statutes are what determine how much if any of your IRA accounts are safe from creditors in a bankruptcy case, said James Delaplane, vice president of retirement policy at the Association of Private Pension and Welfare Plans.

For example, in New Hampshire, no form of an IRA is exempt from the bankruptcy estate, according to the Investment Company Institute, which conducted a state-by-state survey of IRA treatment in bankruptcy. Many states, however, protect at least part of your IRA assets if they are deemed "reasonably necessary for the support of the debtor and any dependents of the debtor."

IRAs in every state, however, may soon receive greater protection from creditors if the Bankruptcy Reform Act in its current form becomes law. IRAs in every state, however, may soon receive greater protection from creditors if the Bankruptcy Reform Act in its current form becomes law.

Final details of the bill are being negotiated, although observers note there is a good chance it may die before reaching the White House. But if it does get through, a proposal of that bill makes it possible for creditors to make claims only on those IRA assets in excess of $1 million. And it would exclude from consideration any assets that had been rolled over from a 401(k) plan, Delaplane said.

Little protection in lawsuits

But the Bankruptcy Reform Act won't make IRAs any less vulnerable in lawsuits.

That's where a pension reform bill currently in Congress may help. It contains provisions that expand the portability of retirement plans, said ICI senior counsel Russell Galer.

Currently, if you roll over money from a 401(k) into an IRA but wish to eventually put it into a new 401(k) plan, you need to set up what's called a "conduit IRA," which is essentially a temporary parking space for your money. If you don't keep that money separate from other IRA funds, you will not be able to move it into a 401(k) plan, Galer said.

If the pension reform bill becomes law, a conduit IRA would not be necessary. Money would be able to move freely between 401(k)s and IRAs. That means you would be able to shelter any of your IRA money in an ERISA-protected plan if you wanted.

The bill also would permit you to transfer money into 401(k)s from nonprofit or state agency plans known as 403(b)s and 457s, something you cannot do at present. ERISA does not protect any 457 plans and only applies to some 403(b)s.

Should you care?

If you're like many people, the threat of being sued for a ransom or crying "Uncle!" financially is not a likely scenario.

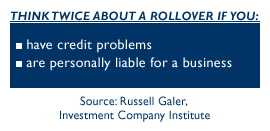

"For the bulk of the American population, it's a relatively minor concern," Galer said.

If, however, you have credit problems or own a small business for which you have personal liability, "you may want to be more careful," he noted, especially if you live in a state that doesn't exempt much if any of your IRA from the bankruptcy estate. If, however, you have credit problems or own a small business for which you have personal liability, "you may want to be more careful," he noted, especially if you live in a state that doesn't exempt much if any of your IRA from the bankruptcy estate.

That's because the consequences of losing your nest egg to creditors are harsh. Not only do you forfeit savings, but if you are under retirement age, you must pay the penalties for early withdrawal, in addition to the income tax on the distributions.

Rollover alternatives

When deciding whether to roll over money into an IRA or keep it in your 401(k), consider the pros and cons ... and the cost, experts say.

"There are advantages and disadvantages to each," said ERISA lawyer Ken Robbett of the law firm Smith & Downey.

When you roll funds into an IRA, "You have complete control over that money," he said. But, he added, "You have less security from [a legal] perspective."

And administratively it may cost you more to maintain an IRA. That's because in a 401(k) you often don't have to pay transaction costs or loads on funds.

Fortunately for many employees, the trend in 401(k) plans is toward more options. So if you are moving to a new job with a better 401(k) plan, one that offers greater variety and sounder investment choices, you might be better off rolling your money directly into that plan.

Consider, too, if your new 401(k) plan offers a brokerage window. That allows you to invest your money outside the plan itself. But, Galer said, "Check out the fees and costs associated with that." You may have to pay a yearly account fee in addition to any commission costs and loads.

Your other choice, of course, is to leave your money where it is if you're satisfied with the plan and its selections.

Whatever you do, experts say, knowing your options in advance of an unanticipated crisis can go a long way toward protecting your assets.

|

|

|

|

|

|

|