|

The hole nine yards

|

|

June 6, 2001: 3:16 p.m. ET

What Krispy Kreme needs to do to ensure its long-term success

By Michael Craig

|

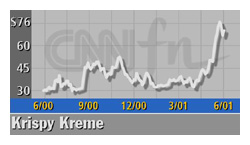

NEW YORK (Business2.com) - It is appropriate that the CEO of Krispy Kreme is named Scott Livengood. In his company's first two weeks on the New York Stock Exchange, Krispy Kreme stock rose from $59 to $75 (which increased its market capitalization to $2 billion), and the company announced its second stock split of the year. Plus, Livengood gets to eat Krispy Kreme doughnuts all day.

But no matter how sweet it seems now, it can all fall apart. For every McDonald's and Starbucks, there are dozens of Boston Chickens, Discovery Zones, TCBYs, and Jiffy Lubes. How can Krispy Kreme and other franchise-driven businesses keep the livin' good?

Krispy Kreme (KKD: up $0.67 to $69.75, Research, Estimates) now has 182 stores, of which about 60 are company-owned. Growth depends on new franchise stores.

In fiscal 2000, 16 new franchise stores opened. That number increased to 25 in fiscal 2001 (which ended January 28, 2001). Six more have opened since January, with another 30 set to open in fiscal 2002.

Area developers (franchisees who buy territorial rights to open multiple locations) are contractually obligated to open 250 new stores between January 2001 and January 2006.

Potential risks for franchise operations

The two biggest potential pitfalls for Krispy Kreme (if we have learned anything from other high-profile franchise failures) are financially assuming risks for its franchisees, and failing to maintain franchisee relationships that make money for both parties. Thin management and over-aggressive expansion plans can compound the risks.

Boston Chicken wrote the book on how to run yourself into Chapter 11 as your franchisees' banker. In its high-flying days, it raised hundreds of millions of dollars, which it used to make its 1,300 franchisees solvent enough to pay royalties (and interest on those loans).

Once investors found out that the actual locations were losing hundreds of millions of dollars, access to capital markets for Boston Chicken dried up, and bankruptcy followed. Jiffy Lube ran into similar trouble with loans.

Krispy Kreme used to have a policy of encouraging employees to become franchisees, offering collateral repurchase agreements and loan guarantees. This policy ended after Krispy Kreme went public.

According to the company's 2001 annual report, its maximum exposure for collateral repurchases is $249,000, and for loan guarantees $600,000. This business of assuming liabilities for franchisees should be a relic of the company's pre-IPO past.

According to the company, it gets 500 calls a week from people who want franchises, so it should have its pick of rich partners. In its April 2000 prospectus, Krispy Kreme declared, "Generally, we do not provide financing to our franchisees."

But after the IPO, Krispy Kreme entered a joint venture (in which Livengood is a 6 percent owner) to develop stores in Northern California. The company owns 59 percent of the venture, but guaranteed 84 percent of the area developer's $4.5 million line of credit.

A 'ruinous' policy

The 2001 annual report disclosed that "from time to time, the company extends credit to franchisees in the form of notes receivable." In addition to the loan guarantees in California, the company had notes receivable outstanding of $3 million in four joint ventures in which it has a minority interest.

With a gigantic expansion in front of it, a continuation of this policy can be ruinous. One of the keys to being successful as a franchisor is to strike the right balance, keeping good relations with franchisees and making it financially lucrative for them to operate, but taking what you can get.

TCBY had poisonous relations with franchisees, who claimed TCBY got greedy with supply-and-ingredient mark-ups. Krispy Kreme, whose directors own 21 stores and whose officers own 13 more, may not get enough from its franchisees.

In early 2000, the company bought back the New York market for $6.9 million from an area developer. That market should have been worth a king's ransom, but the company sold 77 percent of the New York market, including existing operations and future franchise rights, three months later, amidst IPO buzz, for no profit.

This mirrors the way the company has handled Northern California, where, instead of auctioning off this lucrative market, it's stuck putting up equity capital and guaranteeing loans.

Keeping it in the family may not work

Significantly, most of Krispy Kreme's expansion is supposed to come from franchisees who are also insiders. Its officers who are franchisees are contractually committed to opening 171 more stores. It costs $1 million to open a new location. The company cannot put itself at risk financially for its officers.

There is also the question of how profitable it is to own a Krispy Kreme franchise. The places seem like gold mines. But while the company's financial reports don't say as much, there are little hints a franchise may not be as profitable as one would guess.

The company waived one director's Athens, Ga., royalties for the last few years due to operational difficulties; some officer/director franchisee payments to Krispy Kreme have not increased much in the last few years.

It does not bode well that Krispy Kreme's own senior vice president of franchise development, Philip Waugh, couldn't make good on his commitment to open four stores in Kansas City. He opened three stores in four years and the company suspended his obligation to open the fourth.

Krispy Kreme's brand name, rather than its money-raising ability, should be the currency of its expansion effort. The company should recruit people who don't need the company's money or loan guarantees to go into business, not its officers and directors.

And if those wealthy strangers can't open 250 more stores by 2005? Then maybe it's not a good idea for the company to finance.

|

|

|

|

|

|

|