NEW YORK (CNNfn) - European markets moved in tandem with U.S. markets Monday, dipping into negative territory on the heels of pre-warning announcements that sent the Nasdaq lower as Wall Street remains cautious ahead of new key economic data to be released later this week.

With the second quarter nearing a close, players are keyed up for the next batch of profit warnings and eager for clues to the state of the U.S. economy and its impact on business.

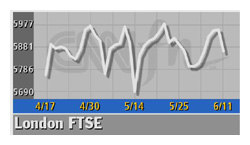

The U.K. FTSE 100 share index closed down 90.10, or 1.51 percent, to 5,860.50 after briefly trading higher on the back of rallying oil and telecoms shares.

The narrower blue-chip DJ Euro Stoxx 50 slipped 24.5 points to 4,4426.5. At that time, the Nasdaq was down 2.5 percent and the Dow Jones industrial average down 0.8 percent.

"The theme has continued to be predominantly negative in European markets flowing warnings from Juniper Networks on Friday. 'Old-economy' cyclicals, defensive stocks, and banks ended the day lower," said Khurtim Chaudhry, equity strategist with Merrill Lynch in London.

Europe's technology shares led the way down, the sector off 2.3 percent overall as (NOK) �fell 3.6 percent while Philips dipped 5.4 percent. �(SI) shed 2.2 percent amid nagging worries about handset sales.

Semiconductor stocks wobbled as U.S. firms Varian Semiconductor Equipment (VSEA: down $3.43 to $39.04, Research, Estimates) and DuPont Photomasks Inc. (DPMI: down $5.94 to $46.06, Research, Estimates) forecast bleak numbers and blamed weakness in the industry.

Telecoms wobble

Telecoms� reversed course to turn lower as heavily weighted �(VOD) shed 3.7 percent, balancing a 1.1 percent gain for Deutsche Telekom.

Finnish operator Sonera slumped 4.5 percent as its chief executive resigned after only six months on the job.

Commerzbank Securities cut its rating on Sonera to "hold" from "buy" to reflect poorer visibility and greater execution risk, adding the news was particularly badly timed given the firm's key development into 3G services.

British bank Lloyds TSB (LLOY) also was among top blue-chip decliners, falling 4.5 percent after a report that it may be ready to walk away from a merger deal with Abbey National because of regulatory opposition.

Abbey fell 5.5 percent. In the same sector, HSBC dropped 3 percent as analysts at SG Securities cut earnings estimates and repeated a "sell" rating.

Energy was stronger, up 0.3 percent as London Brent blend oil prices touched $30 per barrel for the first time since February.

Shell (SHEL) and Royal Dutch (RD) eked out small gains as dealers began worrying about the consequences of Iraq's absence from the market.

Markets poised ahead of new key U.S. economic data, Fed meeting

With bullish corporate news thin on the ground, investors remained cautious ahead of key U.S. data later in the week.

"As for the rest of the week in European markets, U.S. economic data --� retail sales numbers, the CPI numbers, and the U.S. labor market data � are likely to dictate market direction, "Chaudhry said.

"U.S. consumers have remained fairly robust despite an economic slowdown and we're watching to see the growth prospects going forward and to what extent retail sales have been affected."

U.S. retail sales data for May are due Wednesday, followed by the May producer price index and jobless claims Thursday, with the consumer price index, real earnings and University of Michigan consumer sentiment index Friday.

With the next U.S. Federal Reserve interest-rate policymaking committee meeting June 27, investors will be taking a keener interest in the economic data between now and then.

--from staff and wire reports

|